The core takeaway from many personal finance courses, like the Rabbit Habit program, is building a realistic, personalized investment portfolio. This guide details a practical plan for a 31-year-old nurse earning a net monthly income of approximately $2,500 (₩3.3 million) aiming to own a home in the Seoul metropolitan area within 10 years. We'll break down specific savings and investment strategies for this income level.

How Can a Nurse Earning $2,500/Month Build a Realistic Investment Portfolio?

For a 31-year-old nurse with a net monthly income of around $2,500 (₩3.3-3.4 million), constructing a realistic investment portfolio is crucial. While current savings aren't disclosed, living in a low-rent environment (around $75/month or ₩100,000) provides significant room for savings and investment. The first step involves clearly distinguishing fixed costs (rent, insurance, phone bills) from variable costs (food, dining out, transportation). A practical starting goal is to reduce variable expenses, particularly food costs, by about $75 (₩100,000) per month. A sound financial strategy begins with prioritizing savings on payday, then managing living expenses with the remainder. It's also vital to keep an emergency fund covering 3 months of living expenses in a high-yield savings or 'parking' account. Consistent budgeting, whether through an app or a simple notebook, and strategic use of debit and credit cards for year-end tax benefits are smart moves.

What's the Specific Plan for Saving and Investing 50% of Your Income?

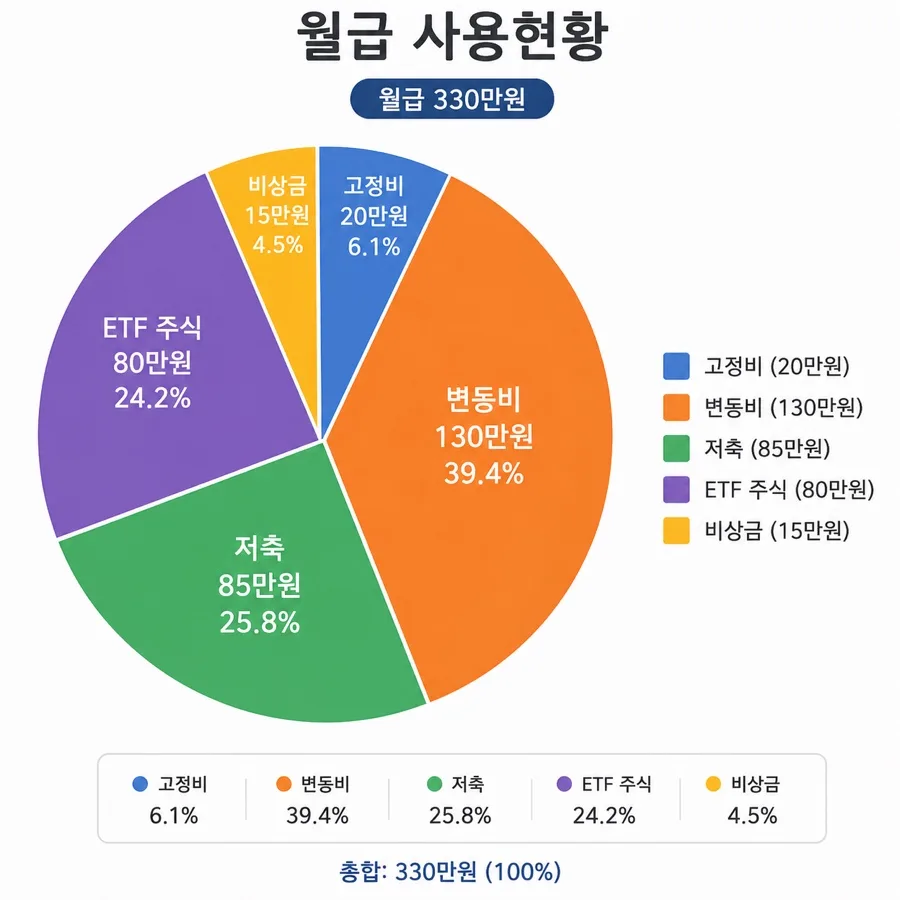

The plan to save and invest 50% of the $2,500 net monthly income ($1,250 total) focuses on minimizing risk with an 'all-weather' investment approach. First, allocate $850 (₩1.1 million) to savings: $800 (₩1.05 million) to high-interest savings accounts (e.g., 7% and 5% rates from specific banks) and $50 (₩65,000) to a youth housing subscription account, a popular Korean savings vehicle for future home purchases. The remaining $800 (₩1.05 million) is dedicated to investments. This includes consistently investing in Exchange Traded Funds (ETFs) through an Individual Savings Account (ISA) and a retirement pension account to maximize tax-advantaged benefits. An ISA allows for tax-free growth up to a certain limit, and retirement accounts offer significant tax deductions. If there are additional surplus funds, consider investing them in U.S. ETFs, which are tax-efficient for annual investments up to $2,500.

What is the 10-Year Roadmap for Homeownership and a Stable Family Life?

A 10-year life roadmap targets homeownership in the Seoul or Gyeonggi Province area and establishing a stable family. Year 1 focuses on building initial capital and dedicated study of investments, alongside establishing a consistent exercise routine to stabilize savings and spending habits. Regularly reading economic news helps in understanding market trends. Years 2-3 involve preparing for marriage with a partner who shares similar values, actively engaging in real estate 'lim-jang' (on-site visits and research), and leveraging accumulated investment knowledge for joint investing. By Year 5, the goal is to purchase a home in Gyeonggi or Seoul and transition from shift work to a standard daytime job for better work-life balance. By Year 10, the aim is to raise children, maintain a stable family, work diligently during weekdays, and enjoy quality time with family on weekends. Secure assets built through consistent investment and diligent work will provide significant peace of mind.

What Were the Key Learnings from the Personal Finance Course and Future Plans?

Taking a personal finance course, such as the Rabbit Habit program, provided a foundational understanding of basic economic terms and concepts previously unknown. Completing practical assignments within the course helped develop a hands-on feel for financial management and fostered a crucial 'I can do this' confidence. The plan is to continue dedicated investment studies, establish a personal investment routine, and work towards long-term financial goals. The guiding principle will be personal growth at one's own pace, rather than comparing progress with others. This steady, consistent approach is key to achieving financial independence and stability.

Tags

💬Frequently Asked Questions

How can a nurse earning $2,500/month start an investment portfolio?

How should I save and invest $1,250 (50% of my income)?

Is homeownership in the Seoul/Gyeonggi area possible within 10 years?

What are the main benefits of taking a personal finance course?

Original Source

Read the Korean original