Starting in 2026, South Korea's Hometown Love Donation program offers expanded benefits, making it financially advantageous to donate. By contributing up to 200,000 KRW (approximately $145 USD), you can receive a significant tax credit, potentially getting back up to 144,000 KRW (around $105 USD) in tax deductions, plus local specialty gifts. This initiative aims to boost local government finances and economies.

What's New with the Hometown Love Donation in 2026?

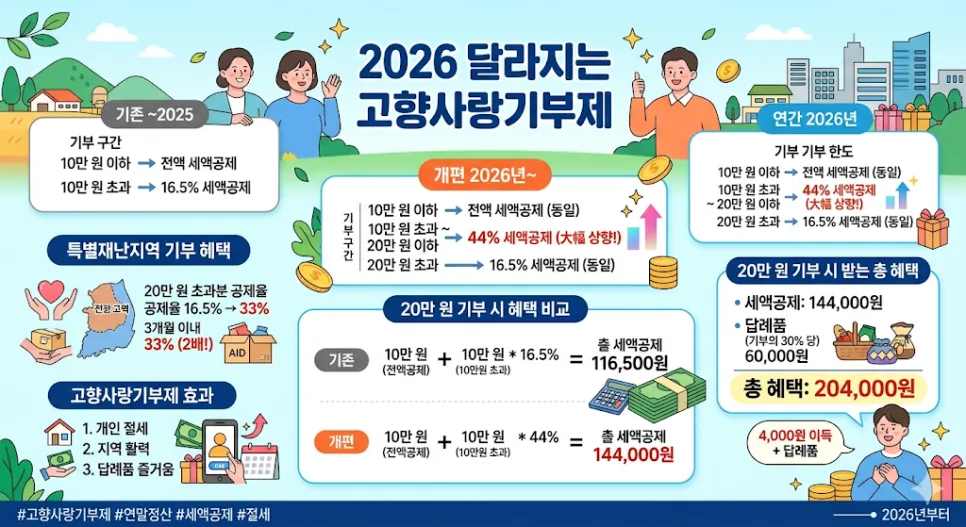

The Hometown Love Donation program allows individuals to donate to local governments outside their primary residence, receiving tax credits and local specialty gifts in return. This system is designed to bolster regional finances and stimulate local economies. A major update for 2026 significantly increases the tax credit rate for donations between 100,000 KRW and 200,000 KRW (approx. $72-$145 USD) from the current 16.5% to 44%. For example, a 200,000 KRW donation previously yielded a total tax benefit of 116,500 KRW (approx. $85 USD) — the full 100,000 KRW deduction plus 16.5% on the next 100,000 KRW. Under the new 2026 rules, this donation will result in a 144,000 KRW (approx. $105 USD) tax credit (full 100,000 KRW deduction plus 44% on the next 100,000 KRW). When combined with the 30% value of local specialty gifts (up to 60,000 KRW or $44 USD), a 200,000 KRW donation can result in a total benefit of 204,000 KRW (approx. $149 USD), effectively giving you a small profit. Additionally, donations to areas declared as special disaster zones will see the tax credit rate for amounts exceeding 200,000 KRW double from 16.5% to 33%, aiding disaster recovery efforts while offering enhanced tax savings. This program has rapidly gained popularity among Korean workers, with annual fundraising exceeding 100 billion KRW (approx. $72 million USD) in its first three years.

How to Maximize Tax Savings with the Hometown Love Donation Program

Related Articles

The Hometown Love Donation program requires you to donate to a local government outside your place of residence. You can choose a region you wish to support, like your hometown, a favorite travel destination, or an area offering appealing specialty gifts. Your donations will be used for local welfare programs, cultural arts, and other community development initiatives. With the 2026 reforms making donations up to 200,000 KRW (approx. $145 USD) financially beneficial due to tax credits and gifts, it's wise to plan this as part of your year-end tax preparation. Popular gifts include high-quality Korean beef (like sirloin), apples, tangerines, black pork sets, freshly harvested rice, and gift certificates from local bakeries. To avoid potential website traffic surges and sold-out gift items, especially near year-end, it's advisable to make your donation in advance. Spreading your donations throughout the year can also help manage cash flow and prevent last-minute rushes, ensuring you don't miss out on valuable tax documentation.

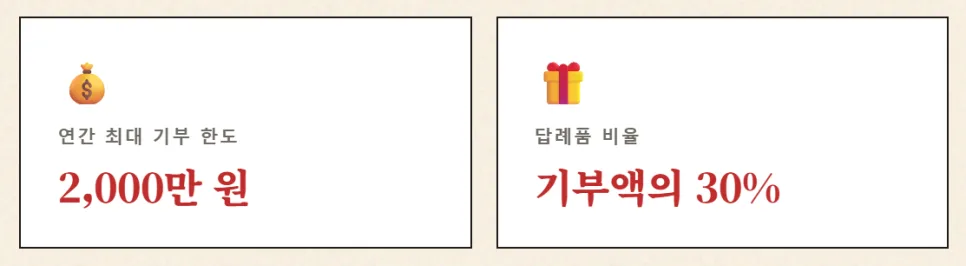

Understanding Donation Limits and Gifts in the Hometown Love Donation Program

As of 2025, the annual donation limit for individuals under the Hometown Love Donation program has been raised to a maximum of 20,000,000 KRW (approx. $14,500 USD) per person. However, the most significant tax benefits are concentrated on donations up to 200,000 KRW (approx. $145 USD). For amounts exceeding 200,000 KRW, the tax credit reverts to the standard 16.5%. The specialty gifts you receive are valued at up to 30% of your donation amount, provided by the specific local government you donate to. For instance, a 200,000 KRW donation allows for gifts valued up to 60,000 KRW (approx. $44 USD). Therefore, donating the 200,000 KRW threshold is the most financially strategic move, maximizing both the 44% tax credit and the gift value. For donations made to areas officially declared as special disaster zones within three months of the declaration, the tax credit rate for amounts over 200,000 KRW increases to 33%, offering an additional layer of tax savings while supporting disaster relief efforts.

This is not financial advice. Consult a licensed financial advisor.