Mastering your first paycheck in 2026 involves a 4-step roadmap from building an emergency fund to investing. Developing sound financial habits early on can significantly impact your wealth over the next decade.

How to Manage Your First Paycheck as a Young Professional?

Stepping into the professional world and receiving your first paycheck is exciting, but it can also bring uncertainty about managing your finances. Don't worry – the financial habits you build as a young professional have a crucial impact on your wealth accumulation over the next 10 years. Many experts emphasize the importance of managing your first paycheck effectively and advise creating a structured plan. A great starting point for effective money management is the '50/30/20 rule.' This guideline suggests allocating 50% of your income to fixed expenses (like rent, utilities, and transportation), 30% to variable spending (entertainment, shopping, dining out), and 20% to savings and investments. For young professionals with lower initial incomes, aiming for a higher savings rate, perhaps 30%, is a worthwhile goal. This approach lays a strong foundation for your financial future.

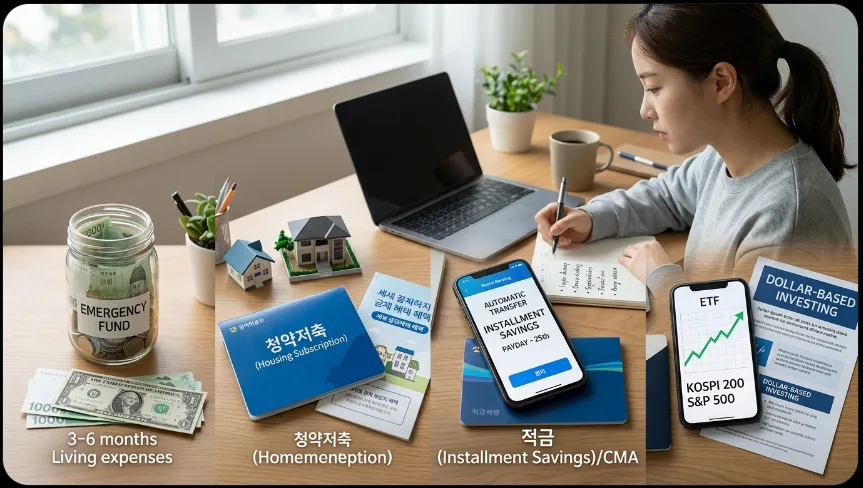

Step 1: Why is an Emergency Fund Your Top Priority?

The first crucial step in successful financial planning is building an emergency fund. It's essential to set aside enough money to cover 3 to 6 months of your living expenses. This fund acts as a safety net for unexpected events like job loss, medical emergencies, or unforeseen accidents. It’s best to keep this money in a high-yield savings account, often called a 'parking account,' or a CMA (Cash Management Account). These accounts offer better interest rates than standard checking accounts while ensuring your funds are easily accessible when needed. Having a robust emergency fund prevents you from having to liquidate investments prematurely during a financial setback, ensuring the stability of your long-term investment strategy. Many experienced individuals stress that securing at least three months of living expenses is the absolute first financial priority.

Step 2: Why is a Housing Subscription Savings Account Essential for Young Professionals?

If you're a young professional, opening a housing subscription savings account should be a top priority. This type of account not only opens doors to future homeownership but also offers significant tax benefits. In Korea, for example, contributing up to 2.4 million KRW (approximately $1,800 USD) annually can lead to a tax deduction of up to 40% (max 960,000 KRW, or about $720 USD) on your income tax return. This directly increases your disposable income. Furthermore, these accounts are structured to benefit long-term savers, meaning the earlier you start, the closer you get to your homeownership goals. Enrolling at the beginning of your career is a financially astute move, providing both housing security and financial advantages. Many young workers successfully use these accounts to achieve housing stability and financial gain simultaneously.

Step 3: How to Build a Savings Habit with a Fixed Deposit Account?

Establishing a consistent savings habit is vital for building financial stability. The most effective strategy is to set up automatic transfers from your main checking account to your savings account on payday. This 'save first, spend later' approach ensures that a portion of your income is consistently set aside before you have a chance to spend it. Simply trying to save whatever is left at the end of the month often proves insufficient for steady accumulation. Start with a basic one-year fixed deposit account, but actively use interest rate comparison apps to find the highest current rates. This practice not only helps you build a substantial nest egg but also instills discipline in your spending and saving habits. This is precisely why financial experts consistently advocate for the 'save first, spend later' method.

Step 4: When and How Should You Start Investing?

Once you've established a steady savings habit, it's time to consider investing to grow your assets. For novice investors, Exchange Traded Funds (ETFs) are highly recommended due to their relatively lower volatility and diversification benefits. Specifically, adopting a 'dollar-cost averaging' strategy—investing a fixed amount regularly, such as monthly, into ETFs that track major indexes like the KOSPI 200 (Korea) or the S&P 500 (US)—allows you to benefit from long-term growth without the stress of timing the market. Even small, consistent investments can lead to significant returns over time due to the power of compounding. However, it's crucial to remember that investing always carries the risk of principal loss. Approach investments cautiously, within your risk tolerance, and choose options aligned with your personal financial goals and risk profile.

Common First Paycheck Management Mistakes for Young Professionals?

Young professionals often make common mistakes when managing their first paychecks. First, using a single bank account for all income and expenses makes tracking finances difficult and can lead to overspending. It's better to establish separate accounts for different purposes. Second, blindly following friends or peers into investments without understanding your own risk tolerance, goals, or the investment itself is a significant error. Always conduct thorough research and ensure the investment aligns with your personal financial situation. Third, using credit card revolving credit ('revolving') services, often justified by 'it's just a small amount,' can be costly. These services can carry annual interest rates nearing 20%, so they should be avoided whenever possible. Recognizing and preparing for these potential pitfalls is key to achieving sound financial management.

For more details, check the original source below.