Building a robust financial defense is crucial for stable asset management, especially in 2026. This guide synthesizes proven strategies for emergency fund preparation and essential insurance coverage, including critical illness plans, to safeguard your finances against unexpected risks.

What's the Right Emergency Fund Size and How Should You Save It?

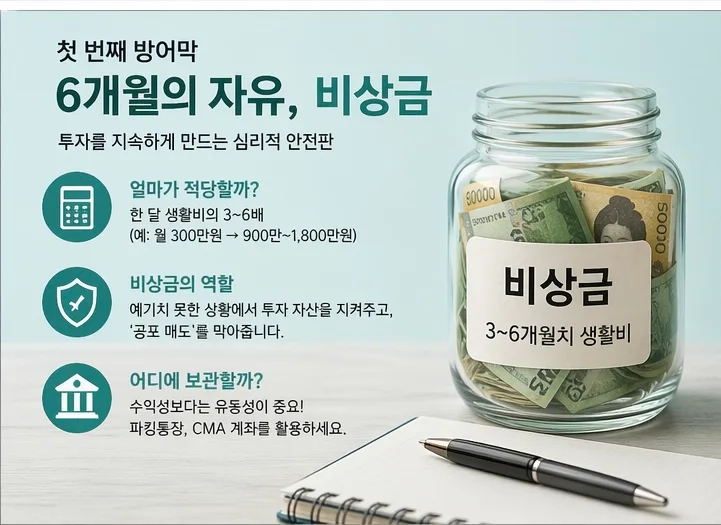

Savvy investors understand that defense is as critical as offense. Unexpected events like accidents, illnesses, or job loss can derail even the most successful investment portfolios. Your emergency fund acts as your strongest shield against these crises, preventing panicked selling during market downturns. Financial experts generally recommend saving 3 to 6 months' worth of living expenses. For instance, if your monthly expenses are around $3,000, aim for an emergency fund of $9,000 to $18,000. Since liquidity is paramount, store these funds in easily accessible accounts like high-yield savings accounts (often called 'parking accounts' in Korea) or money market accounts (CMAs), ensuring you can access them immediately when needed. This fund provides a crucial psychological safety net, enabling you to stay invested through challenging times.

Why Are Health Insurance and Critical Illness Plans Essential?

Insurance isn't the enemy of wealth building; it's your ultimate safety net. Overpaying for insurance can hinder your financial growth, so smart planning is key. The most fundamental coverage is health insurance (like U.S. Medigap or similar plans), which reimburses a significant portion of your medical expenses, making it indispensable. Beyond basic health coverage, critical illness insurance is vital for protection against major diseases like cancer, stroke, and heart conditions. These plans not only cover treatment costs but also provide living expenses during recovery, easing financial burdens. Opting for non-renewable (non-term) policies can lock in your premiums, avoiding future increases. Aim to keep your total insurance premiums within 5-10% of your monthly income. Allocating any remaining funds to direct investments can maximize long-term wealth accumulation.

How Can You Design Cost-Effective Insurance Coverage?

When reviewing or updating your insurance, prioritize cost-effectiveness. The goal is to secure robust coverage without exceeding 5-10% of your monthly income. Focus on pure protection-oriented policies rather than savings-linked ones for better long-term financial growth. Essential coverage includes health insurance (reimbursing actual medical costs) and non-renewable critical illness riders for major diseases like cancer, stroke, and heart attacks. Regularly assess your policies to eliminate redundant coverage and reduce premium costs. Tailor your insurance portfolio to your specific health status, family history, and financial situation to create an optimized plan.

How Does a Financial Defense Impact Long-Term Investing?

Sustained success in long-term investment strategies, such as dollar-cost averaging or dividend reinvestment, hinges on your ability to avoid mid-term withdrawals. Many investors falter not due to a lack of skill, but because they're forced to liquidate assets at market lows due to urgent financial needs. A solid emergency fund and appropriate insurance coverage provide the stability to maintain a long-term perspective, enabling you to continue investing for 10, 20, or even more years. In essence, your 'financial defense' doesn't just protect your assets; it builds the foundation for sustained wealth growth.

Assess Your Financial Defense Today

Building wealth is a marathon, not a sprint. Before embarking on your financial journey, ensure your shoelaces are tied and you have an umbrella for unexpected rain. Tonight, take a moment to review your bank balance: Is your emergency fund adequate? Are you paying for unnecessary insurance premiums? A strong defense fuels effective offense, paving the way for true financial success. Remember, the ideal emergency fund size and insurance coverage vary based on individual circumstances. Consider consulting a financial advisor to build a personalized 'financial defense' strategy.

For more details, check the original source below.