While dividend stocks might seem appealing, they can be inefficient for young investors due to taxes and reduced compounding effects. Reinvesting dividends faces limitations from taxes, cash flow disruptions, and timing challenges, making growth stocks a potentially more powerful strategy for long-term wealth accumulation.

Why Are Dividend Stocks Inefficient for Young Investors?

Many investors enjoy receiving dividends, but it's crucial to understand they aren't 'free money.' Dividends are a portion of a company's profits distributed to shareholders. When a dividend is paid, the stock price typically drops by the dividend amount – a phenomenon known as 'ex-dividend date price drop.' For example, if a stock is trading at $100 and pays a $5 dividend, its price will likely fall to $95 post-dividend. Your total asset value remains unchanged; you've simply converted stock value into cash. For young investors focused on long-term wealth growth, reinvesting these dividends can be less effective than growth stock investing. Each dividend reinvestment is subject to a 15.4% tax in Korea (equivalent to US capital gains tax considerations), and the intermittent cash flow can disrupt the compounding snowball effect. This contrasts sharply with growth stocks, which allow for tax deferral and continuous reinvestment, leading to potentially greater wealth accumulation over time.

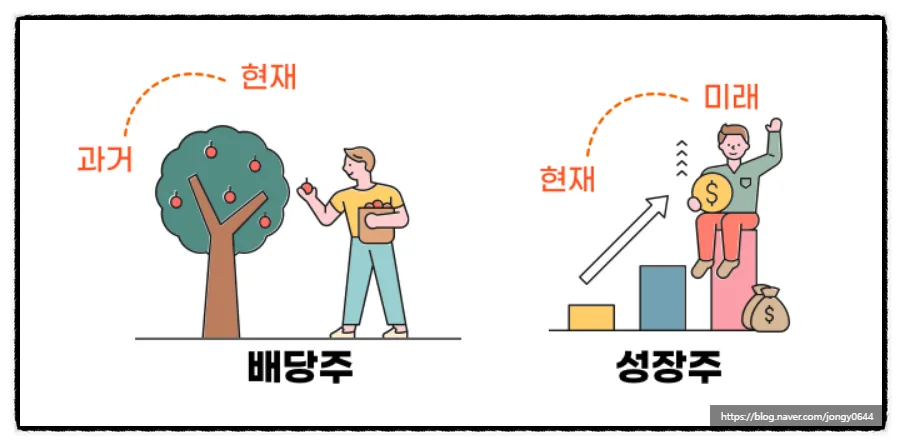

Why Are Growth Stocks Better for Maximizing Compounding?

Growth stock investing focuses on companies that reinvest their earnings back into the business rather than distributing them as dividends. This strategy aims to drive significant stock price appreciation. Investors benefit from tax deferral, as capital gains taxes are typically only paid when the stock is sold. This allows for continuous compounding, where profits are reinvested and generate further profits. For instance, compare investing in a dividend stock yielding 5% annually, where after a 15.4% tax, your net return is around 4.23%, versus a growth stock with an expected 8% annual price increase. Over 20 years, the difference in wealth accumulation can be substantial. A 30-year-old investor starting with $100,000 might see their investment grow to over $200,000 with dividend reinvestment (after taxes), while the same investment in a growth stock could potentially reach $400,000 to $500,000. This significant disparity highlights the power of effective compounding through growth-oriented strategies.

When Does Dividend Investing Become Effective?

Dividend investing isn't inherently inefficient; it becomes a powerful tool during specific life stages, particularly in retirement. When consistent monthly income is needed to cover living expenses, dividend stocks can provide a stable cash flow without requiring the sale of assets. For example, a $1 million portfolio yielding a 4% annual dividend could generate $40,000 per year, or approximately $3,300 per month. This can be a crucial source of retirement income, offering a sense of security and stability amidst market fluctuations. Therefore, the optimal investment strategy is not one-size-fits-all but should be tailored to an individual's age, financial goals, and current circumstances.

What Limits the Compounding Effect When Reinvesting Dividends?

While reinvesting dividends theoretically builds wealth through compounding, several real-world factors can limit its effectiveness compared to growth stock strategies. Firstly, a 15.4% tax is levied on dividends received, reducing the amount available for reinvestment. Secondly, the periodic nature of dividend payments creates cash flow interruptions, breaking the continuous compounding cycle. Unlike growth stocks where earnings are perpetually reinvested by the company, dividend reinvestment requires active management and timing by the investor. These factors collectively hinder the seamless compounding process, making it less efficient for long-term wealth accumulation compared to the sustained growth potential offered by companies focused on reinvesting earnings.

What Should You Consider with Dividend Investing?

When considering dividend stocks, several points warrant attention. Firstly, be aware of the ex-dividend date price drop; your total asset value doesn't increase solely from receiving a dividend. Secondly, understand the tax implications. In the US, qualified dividends are taxed at lower capital gains rates, but non-qualified dividends and interest income are taxed at ordinary income rates. Be mindful of potential 'kicker' taxes or alternative minimum taxes depending on your income bracket and the type of dividends received. Thirdly, thoroughly research the financial health and dividend sustainability of the companies you invest in. Chasing high dividend yields alone can be risky. Ultimately, whether dividend investing is suitable depends on your personal financial goals and situation, making consultation with a financial advisor highly recommended.

For more detailed investment strategies, check the original source below.