When applying for a mortgage, many Americans make the mistake of only checking with their primary bank. However, your main bank doesn't always offer the best interest rate. It's wise to compare average rates using resources like the Consumer Financial Protection Bureau (CFPB) or bank association portals before committing.

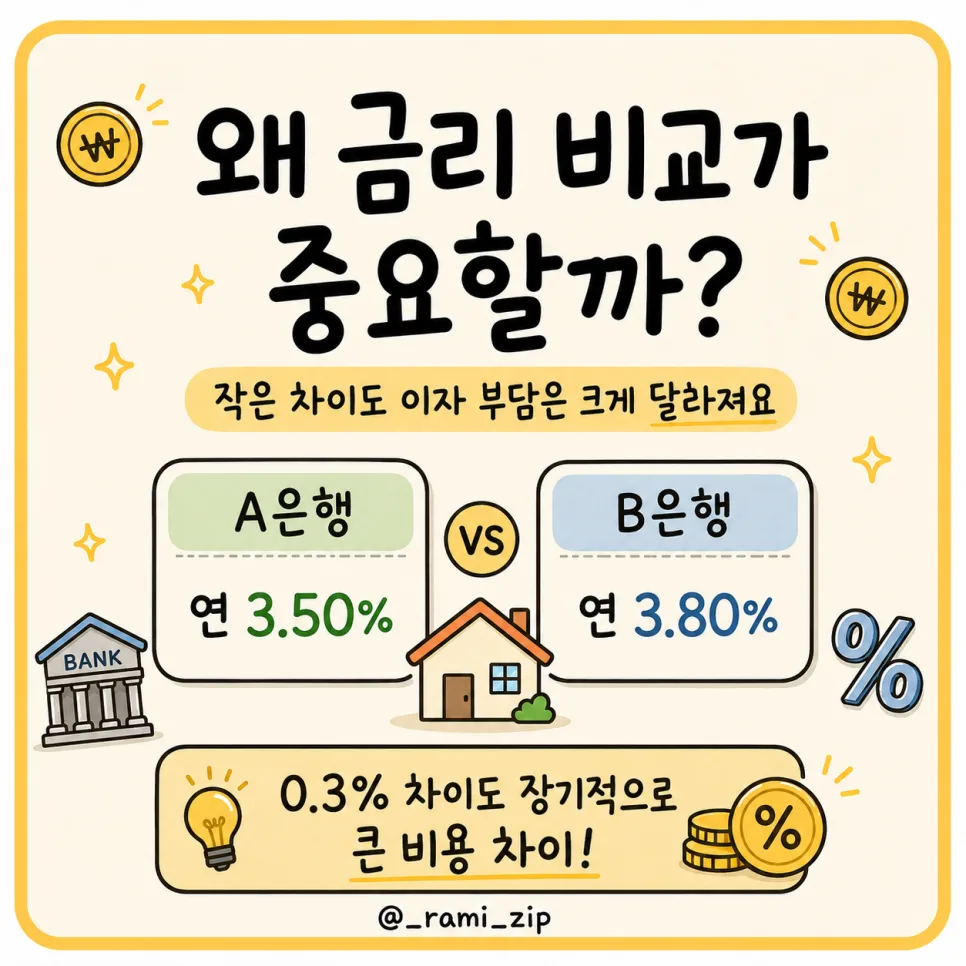

Why Compare Mortgage Rates?

For large, long-term loans like mortgages, even a small difference in interest rates can add up to thousands of dollars in extra interest payments over the life of the loan. For example, a 0.5% difference on a $300,000 mortgage could mean paying an extra $1,500 per year in interest. This is a simplified calculation, and the actual difference can be even larger depending on the repayment method and loan term. Therefore, carefully comparing the interest rates offered by different lenders is crucial for reducing your long-term financial burden.

What is the CFPB Mortgage Comparison Tool and How to Use It?

The Consumer Financial Protection Bureau (CFPB) offers a valuable tool on its website that allows you to compare average interest rates and fees for various mortgage products. This helps you understand the market landscape without visiting each bank's website individually. Before you start your mortgage application, it's highly recommended to check this resource. Simply search for the 'CFPB mortgage comparison tool' online, navigate to the mortgage section, and select the type of loan you're interested in (e.g., fixed-rate mortgage, adjustable-rate mortgage). This will provide a snapshot of current market offerings.

Key Considerations When Comparing Mortgage Rates

The interest rates you find on comparison websites are typically average rates. The final rate you'll be offered depends on several personal factors. These include your credit score, income level, the value and type of property you're purchasing, the loan amount you need, your chosen repayment method, and your existing debt-to-income ratio (DTI). Therefore, use the average rates as a reference point and always get personalized quotes during actual consultations. If the rate offered during a consultation is significantly higher than the average, it's a strong indicator to explore other lenders.

Why You Shouldn't Solely Rely on Your Primary Bank

Just because you've banked with an institution for a long time doesn't guarantee you'll get the best mortgage rate. Banks' funding costs, internal product policies, and customer loyalty programs change frequently. These factors, combined with your individual financial profile (credit score, income, DTI), determine your final interest rate. For a significant loan like a mortgage, it's essential to consult with at least 2-3 different lenders beyond your primary bank. This comparison shopping is key to finding a more favorable interest rate and loan terms, ultimately saving you money.

For more details, check the original source below.