For US investors in 2026, CMA (Cash Management Account) and Parking Accounts (high-yield savings accounts) both offer ways to earn interest on idle cash, but they serve different primary purposes. CMAs, often offered by brokerages, are ideal for managing funds earmarked for investments, offering daily interest and integration with trading platforms. Parking accounts, typically from banks, are better suited for everyday expenses and emergency funds due to their accessibility and deposit insurance.

What's the Core Difference Between CMA and Parking Accounts?

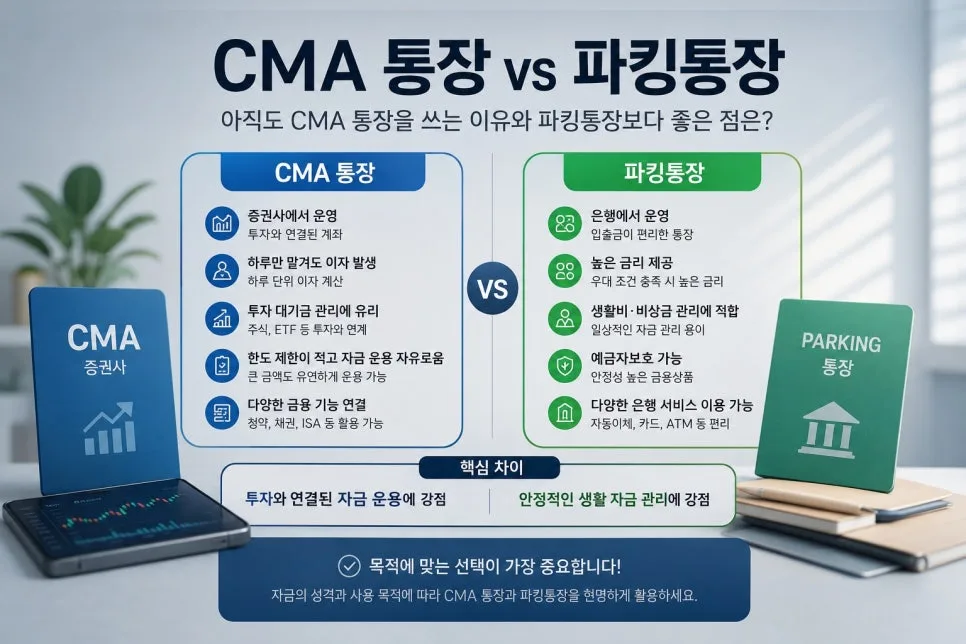

While both CMA and Parking Accounts help your cash earn interest, their fundamental differences lie in who offers them and their intended use. CMAs are primarily offered by securities firms (brokerages) and are designed as investment-oriented accounts. They're perfect for holding cash that you plan to invest soon in stocks, ETFs, or bonds, allowing you to earn interest while waiting for the right market opportunity. Parking accounts, on the other hand, are standard savings accounts offered by traditional banks. They focus on providing easy access for daily expenses, emergency funds, or short-term savings goals, often with competitive interest rates. The way interest is calculated can also differ; CMAs frequently calculate interest daily, making them efficient for very short-term cash parking, whereas parking accounts follow typical bank interest accrual periods. Crucially, deposit insurance coverage varies significantly between the two.

Why Do Many US Investors Still Prefer CMAs?

CMAs continue to be a popular choice for many US investors for several compelling reasons. Firstly, they excel at managing investment cash. If you're holding cash waiting to buy stocks, ETFs, or other securities, parking that money in a CMA allows it to earn interest instead of sitting idle. This is particularly beneficial in volatile markets where you might be observing before committing funds. Secondly, the daily interest accrual is a significant advantage. Even if you only hold funds for a few days between receiving a paycheck and paying bills, or between selling an investment and buying another, a CMA can generate small but consistent interest earnings. This maximizes the efficiency of short-term cash. Lastly, CMAs often have higher balance limits or fewer restrictions compared to some high-yield savings accounts that might cap their best rates at a certain balance or require specific direct deposit conditions. This makes them suitable for larger sums of money being held temporarily.

How Can CMA's Brokerage Integration Be Leveraged?

A major advantage of CMAs is their seamless integration with a brokerage's broader financial ecosystem. Beyond just holding cash, a CMA account typically allows you to trade stocks, ETFs, mutual funds, and bonds directly from the same platform. This consolidation simplifies your financial management, eliminating the need to transfer funds back and forth between a bank and a brokerage account. Many CMAs also offer features like check-writing privileges or debit cards, further enhancing their utility. For investors looking to manage their entire financial portfolio—from cash reserves to active investments—in one place, the integrated nature of a CMA offers significant convenience and efficiency. It turns your cash account into a more active part of your wealth-building strategy.

When is a CMA More Suitable Than a Parking Account?

While CMAs offer distinct advantages for investors, parking accounts (high-yield savings accounts) are often a better fit for different financial needs. If your primary goal is to manage everyday living expenses, such as paying bills, receiving your salary, or setting up automatic payments, a bank-offered parking account is generally more convenient due to its direct integration with the banking system. Most reputable parking accounts are also FDIC-insured, meaning your principal and earned interest are protected up to $250,000 per depositor, per insured bank, for each account ownership category. This provides a high level of security for your funds. In contrast, not all CMAs are FDIC-insured; some, like those based on repurchase agreements (RPs), carry investment risk and could result in a loss of principal. Therefore, if prioritizing absolute safety and ease of daily transactions is key, a parking account is likely the superior choice.

What Are Key Considerations When Using a CMA?

When considering a CMA, it's crucial to be aware of a few key points. The most important is to verify the deposit insurance status. Not all CMAs are FDIC-insured. Some types, such as those offered by money market funds or repurchase agreements (RPs), are not covered by FDIC insurance and carry inherent investment risks, meaning you could lose money. Always check the specific details of the CMA you are considering. Furthermore, while CMAs offer convenience for investors, they might not be the most user-friendly option for everyday banking compared to a traditional checking or savings account. For instance, check-writing features might be less common or have limitations. It's essential to align your choice of account with your primary financial goals—whether that's maximizing investment liquidity and potential returns or ensuring the utmost safety and accessibility for your daily funds. Carefully weigh the pros and cons of both CMAs and parking accounts based on your personal financial situation and risk tolerance.

For more details, check the original source below.