You can secure up to $200,000 in accident disability coverage for about $7 per month by strategically selecting specific insurance riders. This is particularly feasible for individuals aged 59 with lower-risk occupations like homemakers or office workers, offering a high coverage-to-cost ratio that's considered a great value. This guide breaks down how to achieve this coverage, calculate benefits, and what to look out for before signing up, updated for 2026.

What is Accident Disability Insurance and Why Is It Crucial?

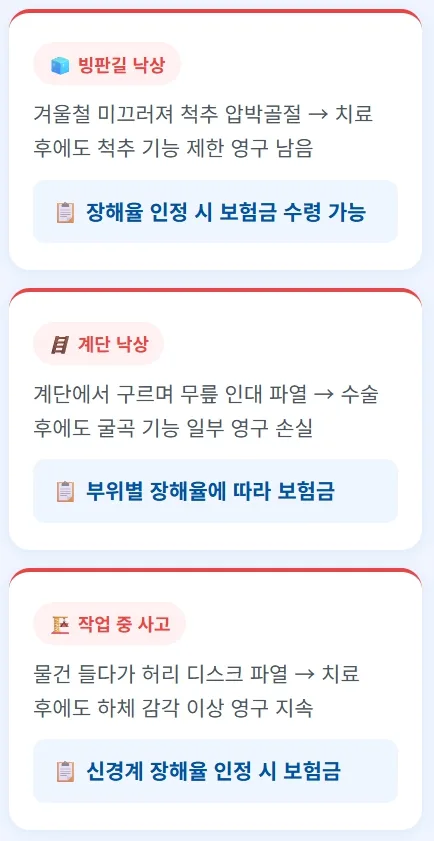

Accident disability insurance, often referred to as a 'permanent disability rider' in the US, provides financial support if you suffer a permanent physical impairment due to an accident. This can range from a fall on an icy sidewalk to a minor car crash. While many Americans prioritize cancer or general health insurance, they often overlook this rider, which can offer substantial coverage – up to $200,000 – for a minimal monthly premium. For instance, a 58-year-old homemaker might experience lasting back issues after a fall, only to realize her existing policies don't cover the long-term functional limitations. It's vital to understand that benefit payouts are based on an objective disability rating determined by a doctor, not just subjective discomfort. In the US, a disability rating of 3% or higher can qualify for benefits under certain policies, a lower threshold than many people assume.

How Are Accident Disability Benefits Calculated in the US?

Accident disability benefits are calculated by multiplying your chosen coverage amount by the assessed disability percentage. For example, if you have $200,000 in coverage and are assessed with a 10% disability rating, you would receive $20,000 in benefits. The disability percentage is determined by a medical professional based on the specific injury and the terms outlined in the insurance policy's disability classification schedule. Factors such as the affected body part, the severity of the impairment, and the potential for recovery are all considered. While not all policies are identical, common qualifying events can include disc injuries from falls, fractures from car accidents, or other permanent physical limitations, even if surgery isn't required. It's essential to consult your policy's fine print and discuss any potential claims with your insurer.

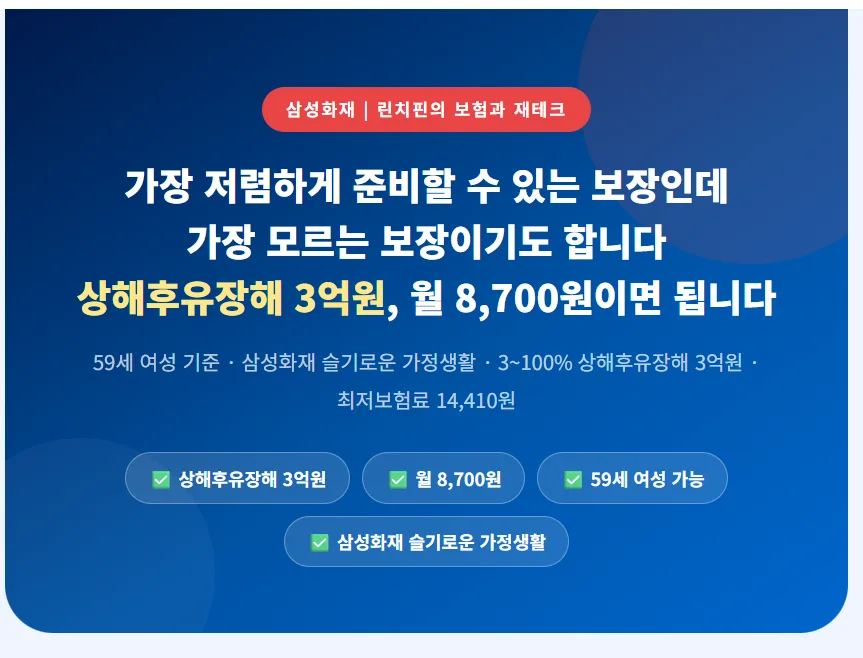

Achieving $200K Accident Disability Coverage for Around $7/Month: A Real-World Example

Securing $200,000 in accident disability coverage for approximately $7 per month is achievable through specific riders, often found with major insurers like Samsung Fire & Marine Insurance (though US equivalents would be companies like State Farm or Allstate offering similar riders). For a 59-year-old female in a low-risk occupation, such as a homemaker or office worker, this premium is possible when bundled with a primary policy that requires a minimum death benefit, for instance, $30,000. The lower premium for these roles is due to a lower 'occupational class' rating, which directly impacts insurance costs. It's important to note that if your occupation changes to something with a higher risk, you must inform your insurance provider, as this could affect your premium. For women in their 50s and 60s, this coverage is particularly relevant due to increased risks of falls and potential complications like hip or spinal fractures, which can lead to lasting mobility issues.

Key Considerations Before Purchasing Accident Disability Insurance

Before committing to an accident disability insurance policy, it's crucial to review any existing insurance coverage you have. Check if you already have a similar disability rider and understand its coverage amount and terms. Overlapping coverage can lead to unnecessary expenses. Additionally, carefully read the policy documents to understand the specific criteria for disability assessment and benefit payouts, as these can vary significantly between insurers. Since this falls under YMYL (Your Money Your Life) categories, making an informed decision is paramount. Consider consulting with a licensed financial advisor or insurance broker to ensure the policy aligns with your personal financial situation, health status, and long-term goals. This ensures you're not overpaying for coverage you don't need or underinsured for potential risks.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in Accident Disability Insurance: $200K Coverage for $7/Month (2026)?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original