The 5th generation of Korean private health insurance (실손의료보험, Silson Uiryo Boeom) in 2026 significantly lowers premiums by up to 50% compared to the 4th generation. This is achieved by reducing coverage for non-critical, non-insured (비급여, bi-geupyeo) treatments and increasing the patient's out-of-pocket responsibility to 50%, while enhancing coverage for critical illnesses.

Will 5th Gen Korean Health Insurance Premiums Be Lower in 2026?

A major characteristic of the 5th generation Silson Uiryo Boeom is a substantial reduction in premiums compared to the 4th generation. By decreasing coverage for unnecessary non-insured benefits, the basic premium burden is significantly lightened. Specifically, if you opt for only the rider for critical non-insured treatments (Special Rider 1), premiums can be up to 50% lower than the 4th generation. Even if you include the rider for non-critical non-insured treatments (Special Rider 2), you can expect a premium reduction of about 30%. However, similar to the 4th generation, the individual-based differential pricing system, where premiums are discounted or increased based on the previous year's non-insured treatment usage, remains in place. This reflects the insurers' intention to curb excessive medical utilization.

How Are Non-Critical Non-Insured Benefits Reduced? (Out-of-Pocket Responsibility Increased to 50%)

Under the 5th generation Silson Uiryo Boeom, the patient's out-of-pocket responsibility for non-critical non-insured treatments, such as those for common ailments like colds, body aches, or back pain, has increased. The most notable change is the rise in the out-of-pocket deductible from 30% to 50%. For example, if a non-insured treatment costs $1,000 USD (approximately ₩1,300,000), under the previous system, you would pay $300 USD (₩390,000), but with the 5th generation, you'll pay $500 USD (₩650,000). Furthermore, the annual coverage limit for non-critical non-insured benefits has been drastically reduced from $38,000 USD (₩50 million) to $7,700 USD (₩10 million). For inpatient treatments of non-critical conditions, the maximum payout per instance is capped at $2,300 USD (₩3 million), increasing the financial burden for prolonged treatments. These measures are interpreted as steps taken by insurance companies to manage their loss ratios.

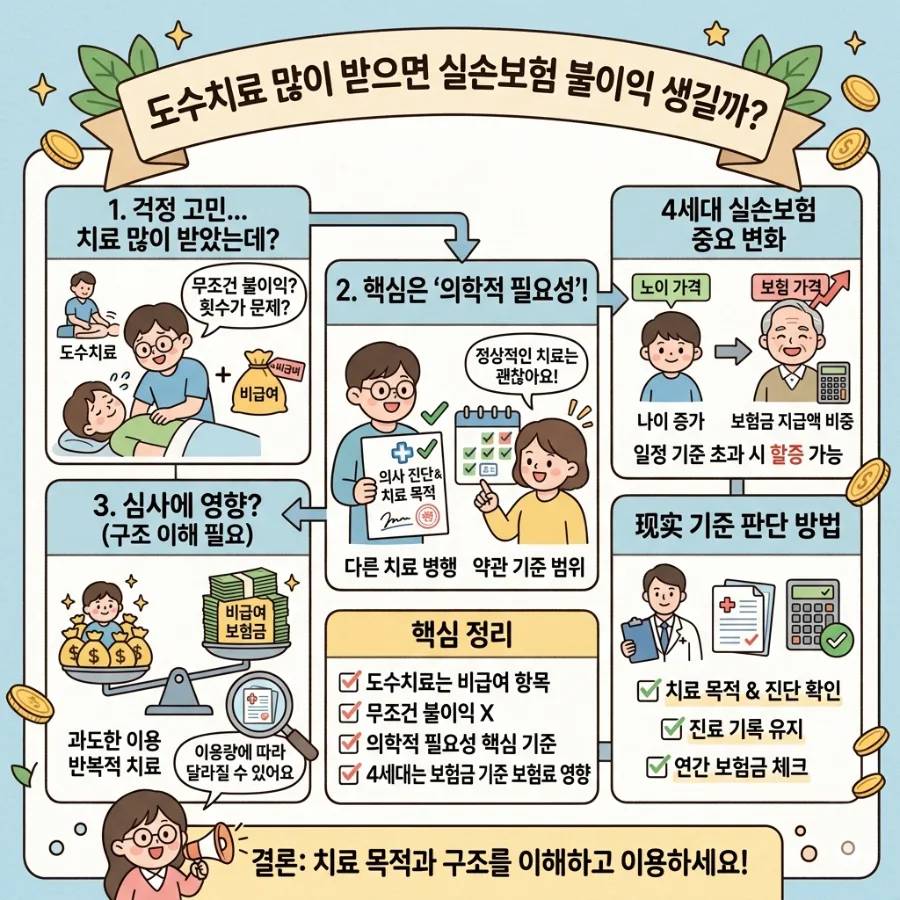

Are Manual Therapy and Non-Insured Injections Covered for General Conditions?

Treatments like manual therapy and non-insured injections, previously identified as major contributors to excessive medical spending, are now largely excluded or significantly reduced in coverage for general conditions. If you receive such treatments for non-critical illnesses, coverage will be difficult to obtain, or the out-of-pocket cost will be very high. MRI scans are also subject to a reduced annual limit of $1,500 USD (₩2 million) under the 5th generation, down from $2,300 USD (₩3 million) annually in the 4th generation. However, this applies only to general conditions. If manual therapy or non-insured injections are administered for critical illnesses such as cancer, cerebrovascular diseases, or heart conditions, they will still be covered with the same 30% out-of-pocket deductible as in the 4th generation. This serves as an exception to maintain treatment accessibility for critically ill patients.

Is Coverage for Major Illnesses (Critical Conditions) Enhanced?

While coverage for general conditions has been reduced, the 5th generation Silson Uiryo Boeom enhances coverage for critical non-insured treatments like cancer, cerebrovascular, and heart diseases. When receiving inpatient treatment at facilities like comprehensive hospitals, any amount exceeding $3,850 USD (₩5 million) of the annual out-of-pocket expenses will be additionally supported by the private health insurance. This acts as a crucial safety net designed to reduce the risk of financial ruin for patients facing high treatment costs for critical illnesses. Therefore, it is designed to significantly alleviate the medical expense burden in case of a critical illness diagnosis.

Are Benefits for Pregnancy, Childbirth, and Developmental Disorders Newly Included?

Items related to pregnancy, childbirth, and developmental disorders, which were previously difficult to cover under existing private health insurance, are now newly included and covered under the 5th generation Silson Uiryo Boeom. Specifically, coverage is now available for 'insured' (급여, geupyeo) items related to pregnancy and childbirth, such as prenatal check-up costs and delivery expenses, as well as 'insured' treatments for developmental disorders. This initiative aims to expand medical support in areas of growing social importance.

Why Is the Insured Benefit Deductible Differentiated by Hospital Size?

To mitigate the trend of patients flocking to larger hospitals over local clinics, the 5th generation Silson Uiryo Boeom has differentiated the out-of-pocket deductible for insured benefits based on hospital size. Local clinics will have a 30% deductible, hospitals will have a 40% deductible, general hospitals will have a 50% deductible, and comprehensive hospitals will have a 60% deductible. This policy change aims to streamline the healthcare delivery system and prevent patients with mild conditions from unnecessarily using higher-level medical facilities. Consequently, it has become more important for patients to choose the appropriate medical institution based on their symptoms.

For more details, check the original source below.