Considering the upcoming 5th generation of South Korea's private health insurance (Silson), understanding the potential premium reductions versus coverage limitations is crucial. Set to launch in May 2026, this new policy tier introduces significant changes to out-of-pocket expenses for certain treatments, making it essential to review these points before enrolling.

What's the biggest change in the 5th Gen Korean Health Insurance?

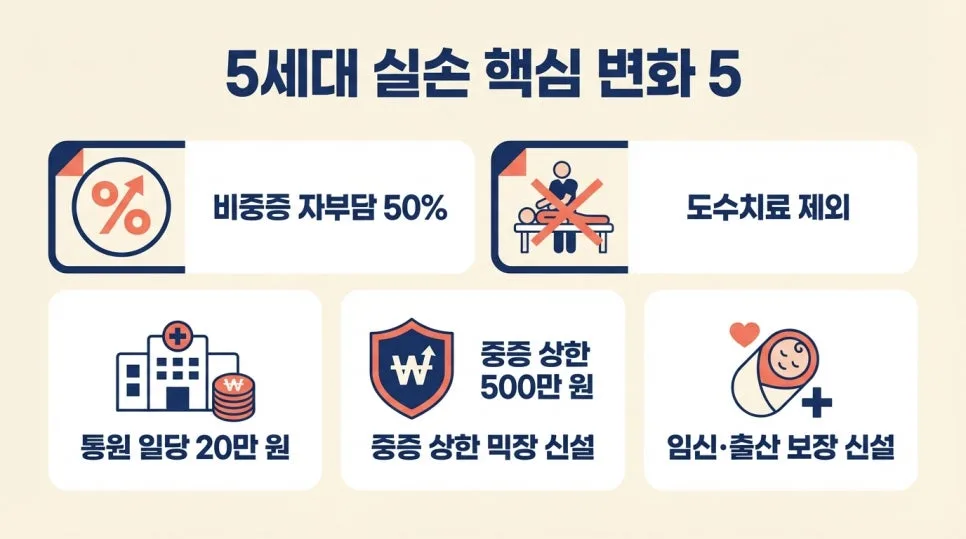

The most significant shift in the 5th generation of Korean health insurance lies in the reclassification of non-covered (non-급여) medical services into two categories: 'severe' and 'non-severe.' According to the Financial Services Commission's proposed guidelines, treatments for severe conditions like cancer and heart disease will maintain or even see enhanced coverage. However, frequently used non-severe treatments, such as physical therapy or non-covered injections, will face a higher 50% co-payment and reduced coverage limits. This adjustment aims to curb over-utilization of non-severe treatments, which have been a major driver of rising insurance payouts. Therefore, identifying whether your common non-covered treatments fall into the severe or non-severe category is a key factor when deciding on the 5th generation plan.

How much will premiums decrease and coverage change with 5th Gen Korean Health Insurance?

Related Articles

Switching to the 5th generation of Korean health insurance can lead to noticeable premium savings. For a 40-year-old male, while 4th generation premiums might range from approximately $11-$15 USD per month, the 5th generation could potentially lower this to the low $10s USD, offering annual savings of around $40 USD. Coverage for severe non-covered treatments will retain an annual limit of approximately $37,000 USD, and a new out-of-pocket maximum for inpatient care at tertiary hospitals may reduce the burden for major illnesses. However, coverage for non-severe non-covered treatments will see a rise in co-payment to 50%, with new limits such as $150 USD per day for outpatient visits and $2,200 USD per instance for inpatient care at clinics/hospitals. This contrasts with the 4th generation's per-instance outpatient limit of $150 USD, meaning visiting multiple clinics on the same day might result in less coverage under the new system.

How do co-payments for outpatient visits change in the 5th Gen Korean Health Insurance?

Another key change in the 5th generation of Korean health insurance affects the co-payment structure for covered outpatient services. Under previous generations (up to the 4th), the co-payment for outpatient care was a mix of fixed amounts and percentages, resulting in relatively consistent out-of-pocket costs regardless of the facility. The 5th generation, however, links these costs directly to the national health insurance co-payment rates. This means that using higher-level facilities—such as general clinics (30% co-pay), hospitals (40%), comprehensive hospitals (50%), and tertiary hospitals (60%)—will result in a proportionally higher co-payment from your private health insurance. Consequently, seeking treatment for common ailments like colds at a top-tier hospital could lead to reduced reimbursement from your 5th generation plan. It's advisable to consider your typical healthcare provider choices when deciding whether to switch.

Will existing Korean health insurance policyholders be forced to switch to the 5th generation?

There's a misconception that existing policyholders will be mandated to switch to the 5th generation of Korean health insurance. This is not the case. Individuals with 1st generation policies or 2nd generation policies purchased before April 2013 are not subject to mandatory conversion due to their policy terms. However, it's important to note that premiums for these older policies may continue to increase. Policyholders of 2nd generation plans purchased after April 2013, as well as 3rd and 4th generation policyholders, have the option to maintain their current coverage or switch to the 5th generation. It is crucial to verify your specific policy's purchase date and coverage details rather than relying on rumors. Consulting with a financial advisor is recommended to make an informed decision based on your personal circumstances.

For more detailed information, check the original source below.